Articles

13 Rules of ICO Investing

One of the biggest use cases of cryptos besides Bitcoin has undoubtedly been ICOs (initial coin offerings) which allows anyone from anywhere in the world to easily raise money for a blockchain based venture and provide liquid tradeable tokens to investors that often represents a currency on the platform. This trend really exploded in the summer of 2017 and reached a peak in early 2018 with money raised totaling $6.3 billion in Q1 alone. Despite it falling off in recent months, it’s not something that’s going to just disappear due to the easy way in which it allows for venture capital and startups to effortlessly meet in a digital world. While investing in the right ICOs have resulted at times in incredible gains at times surpassing 100x returns within a calendar year, other such investments have actually ended up terribly with investors losing a huge chunk of their capital. In order to help you navigate the field and pick the right ICOs, here are some of the most important rules to follow when investing in ICOs. They won’t guarantee that you’ll stumble upon a winner, but it will most certainly reduce your chances to falling prey to many of the mistakes people make when putting their money in ICOs.

ICO investing has exploded in the last year…which has brought with it many risks.

Rule #1: Understand The Risks

This might sound a bit obvious as there’s a level of risk involved in pretty much any investing, but you won’t know true risk until you get yourself involved in the world of cryptocurrencies and especially ICOs. The things that happen in this space is mind-boggling and often times ridiculous, you’ll at times wonder how any of it is possible in this day and age when you’d think there should be rules and regulations to prevent some of this seedy behaviour from taking place. This is in fact why we started this website in the first place, to shine a light and do our best to help folks navigate the wild west of tokenized assets.

The above image looks like a transparent and investable team, except it’s not even real.

What do we mean by risks besides a very real chance that your investment could lose 90% of its value under a year? The team could have fake profiles like Benebit (pictured above), they could drastically switch the terms of their ICO like Mercury Protocol after launch, they can increase their hard cap after reaching a level of popularity like Enigma, they could cancel their ICO after a lengthy vetting process like Gems Protocol, or well…they could just exit scam with the money like dozens of projects do every month. You might be wondering why even participate in any ICO if the space is riddled with such shady behaviour, and the simple answer is that it is such risk that allows the few winners to post life-changing returns as is the case of successful ICOs like Ethereum, Neo, and Stratis just to name a few.

Rule #2: Realize You’re Investing In The Team

While ICOs are selling you on a revolutionary future and making all sorts of promises about their product, what you’re really investing in when you put money in ICOs is the team. Given that the ICO investment space is still largely unregulated and investments at max come with a loosely binding SAFT (Simple Agreement for Future Tokens), you really have to trust that the team is going to do right by the investors. Obviously an anonymous team is an absolute no-no and clear links to each team members LinkedIn or equivalent pages are a necessity so you can do your due diligence.

Different people have different methods for evaluating the team but past performance is indeed the best indicator of future performance in this case. You may think that the 19 year old CEO with no work history could be the next Vitalik Buterin, chances are he’s not and you’ll already be needlessly exposed to a gamble when there are already so many other facets of the investment that involve much risk which you can’t actually control. Another risk is picking teams from specific regions like Eastern Europe or China where the regulatory, business, and ethical frameworks are not as transparent or developed, and thus there’s increased chance of getting burned.

Dan Larimer’s success in previous crypto projects was one of the predominant reasons why investors were happy to give him billions when he launched the EOS ICO.

A mix of experience working on blockchain related projects and a link to the real business world where the project is going to be operating is the ideal mix. Often times you have an over concentration of one or the other and that will lead to either not enough development or not enough business development, both of which will lead to a project’s downfall. A leader that has proven entrepreneurial skills and built and exited a successful startup goes a long way.

Rule #3: Analyze The Advisor & Promoter Choices

While the intentions and mindset of the team might be hard to decipher based on looking at their resume, the way in which they go about picking advisors and influencers will be a very clear signal as to what kind of project you’re dealing with. ICOs that are looking for a quick raise and exit are much more likely to hire advisors that have short term benefits like ICO influencers and well-respected business folk that at first seem to lend the project legitimacy but you soon realize have their name tagged to dozens of ICOs and are basically just cashing in without providing much added value. We won’t call anyone out but stick around for a while and you’ll know exactly who these people are.

Paris Hilton promoting a shady project founded by a man convicted of domestic violence was the peak of the ICO bubble.

Another huge red flag that almost single-handedly should see you running for the exit is when ICOs use celebrities to promote their coins. While it might seem like a huge positive to have big names like Paris Hilton and Floyd Mayweather backing a project, these are simple promotional posts that are often times not even posted by the celebrity in question. Steven Segal even went on to promote a blatant scam ICO called, we shit you not, Bitcoiin with two i’s that unsurprisingly ended up being a pyramid scheme.

Rule #4: Make Sure The Price Is Right

Even the sounding ventures can be worth a punt when priced low enough and even the best sounding projects won’t make for a good investment if priced too high. The market cap of the project is the figure that’s looked at when evaluating this metric and it’s calculated by multiplying the ICO price of the token by the total amount of circulating tokens (funnily enough the total token supply is largely ignored in the space).

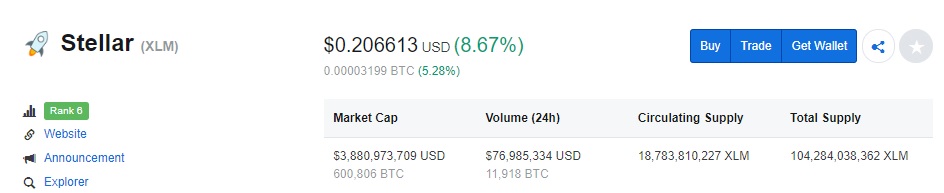

Currently Stellar Lumens has a higher implied market cap (when factoring in total supply) than even Ethereum, but market only seems to care about circulating supply.

What constitutes the right market cap from an investment standpoint has actually very little to do with how much the team really needs to execute their vision but more to do with the state of the market (whether we’re in a bull or bear market trend) and the type of project that the ICO is building. Infrastructure projects which are building new blockchains or new protocols tend to command a higher valuation in the market compared to projects that are building dApps (decentralized apps) on an existing platform like Ethereum.

For example in a down market, even $10 million might be too much for a dApp regardless of how amazing it sounds (eg: a decentralized Airbnb) while in a bull market investors won’t bat an eye throwing $50 million+ at a new “next-generation 3.0/4.0” blockchain project. Some really hot projects, usually with some kind of Silicon Valley backinglike Filecoin or perhaps existing companies with a popular product like Telegram can raise in the hundreds of millions or even billions. These type of investments have historically not had the greatest ROI so keeping it at under $50m for a great infrastructure project and less than $15m for a dApp is a good bare maximum when considering the amount raised.

Rule #5: Project Vision/Idea Aligning With The Team & Trends

Normally the idea behind a project is the first and nearly only thing that a newbie investor will consider, but in our view it holds much lesser importance. The first question that should be asked is whether the project really needs to be on the blockchain or be decentralized, the wrong answer here and the investment case no longer exists. But beyond that we already highlighted in rule #4 that the scope of the project is more important in investor’s eyes during the speculative stage than the specific business idea itself. In terms of the specific idea, it’s more important in the short term that the market, regulatory, and business trend is aligned with the idea. For example a decentralized exchange project might be deemed attractive if we’re in a period where centralized exchanges are struggling or getting shutdown and not many alternatives exist, but much less so if there are already countless decentralized ICO projects and centralized exchanges are thriving (as is the case today). Ultimately, projects that are tackling immediate problems are more likely to do well than projects looking for a solution to inexistent problems or just providing a small improvement to current existing options.

Theta is building a next generation video delivery solution but probably no one would care if they didn’t have the matching personnel.

From a more long term perspective, the execution of the idea has a much better chance at being successful if the team and advisors around the project are seasoned veterans in the specific field where they’re trying to apply a blockchain based solution. For example the crypto credit card project STK did not fare very well in the short term as the crypto card trend died down heavily following the VISA/Wavecrest shutdowns but they have a better long term outlook because they have a team made up of former banking and credit card execs.

Rule #6: Lookout For Early Investors & Bonuses

When you hear the phrase “initial coin offering” you might be thinking you’re getting in at the ground floor, but that’s usually far from the case. Depending on when the project started its funding, there could be venture capital investors that got in way before you and have secured tokens at a much discounted rate. There’s also tactics used like a pre-sale period which is more aimed at influencers or crypto hedge funds and perhaps a few well connected whales. They too will likely get bonus tokens and essentially be able to invest at a cheaper rate than you.

ICOs that give out large bonuses and use time pressure tactics are largely to be avoided.

While this doesn’t sound like much big of a deal when it’s a raging bull market and everything is mooning, the reality during a bear market is much more harsh. Everyone is much quicker to take profits and people are even happy at times getting out of the investment at breakeven. Their breakeven however, might sometimes be equivalent to you losing half of your investment as their selling push prices down way below your acquisition cost. It’s therefore imperial when participating in an ICO or even a pre-sale to know exactly who got in at how much and at what volume and what the lockups are for such discounted prices.

Rule #7: Make Sure Team, Advisor and Early Stage Investor Tokens Have Lock-up

Following directly from the above, it’s important for all the people who’re getting either ‘free’ or heavily discounted tokens to have a vesting period that ensures they can’t just dump them on the market. Besides protecting investors who got in at higher price, this also ensures that the team has to deliver on their milestones and actually do what they set out to do if they wish for their tokens to have any sort of value. The longer the lock-up, the more confidence you can have that the team believes in what they’re doing. Some teams have such confidence in their project that they will initiate a token buy back program like Blackmoon Crypto and that can give you somewhat of a safety net in case things go south.

Being aware of the lockup periods of the different tokens circulating the market can be really crucial in predicting the demand/supply dynamic.

For smaller projects, it’s even important to look at anyone else who might be getting free tokens like bounty programs or community airdrops. These tokens tend to be insta-dumped on the market regardless of price and not having enough volume will result in a very poor start out of the gate and could cascade into further investor panic.

Rule #8: Favorable Tokenomics & Token Distribution

We’ve covered parts of this throughout the post such as having a decent cap and guaranteeing the bonus and lockups are adequately set, but there’s a few more points here that are worth pointing out. Little things like setting the initial price low enough (such as 1c per token) can have a large psychological impact as many uninformed investors feel that tokens that costs multiple dollars are ‘expensive’ when in fact the market cap is where you’ll see whether a project is overvalued. What percentage of the total tokens are in the hands of the team compared to ICO participants are also worth watching out, especially if you are looking at it from a long term perspective.

Another major factor is the profile of the investor base that managed to get into the ICO. Highly hyped ICOs that saw a huge number of participants like for example 0x ended up doing great as no one party got too many tokens. Recent attempts at trying to manufacture a demand deficit by limiting ICO investors through whitelists and tiny allocations however is starting to be less and less effective. Often times many people are aware what the ‘hot projects’ are and making retail investors jump through hoops like ‘proof of care’ devotions or participating in quizzes only serves to aggregate them. Fairly involving retail investors and not lazily relying on VCs or investor syndicate pools seems to be imperative going forward, especially in a downmarket.

Rule #9: When Exchange?

The phrase “when exchange?” is one of the biggest memes of the ICO world as investors constantly flock ICO telegram groups asking over and over again when the tokens they’ve bought will become liquid so they can sell and get their capital back. It mind sound silly and somewhat short-sighted, but exchanges do play a big role in at least the short to mid term success of a project. A decentralized network needs a community to thrive and allowing the free movement of tokens so new people can come in and existing early adopters are motivated to keep participating plays a big part in community building.

The joke is that there are three important questions for an ICO investor. 1) When ICO? 2) When Exchange? 3) When Moon?

It doesn’t help that the exchange listing process seems to be more of a dark art than a science as some projects seem to be quickly listed as a result of personal connections or maybe the right amount of hype behind them, while others can’t even get listed regardless of accepting to pay the exuberant amount of fees to get listings on the top exchanges. As an ICO investor, since ICOs aren’t really allowed to directly mention exchange plans you kind of have to read between the lines of where your project is going to end up by looking at connections of team members, advisors, and even whether ICO funds have been set aside for this exact purpose. Some teams will openly declare they have no interest in paying any money to get listed in exchanges, and some even have gone as far as discourage exchanges from listing them, and these are projects you should be very careful with unless you don’t mind having your capital locked up for an indefinite period of time.

Rule #10: Having A Clear Roadmap & Timeline For A Working Product

ICO investors are largely an inpatient and restless bunch so a constant stream of news and developments is necessary to keep the spirits and confidence high and prevent early investors from dumping the token and moving on to the next shiny ICO. This is where a roadmap comes in and you’ll want to have a close eye on how detailed the roadmap is and how aggressively the dates have been set. A project that doesn’t have any milestone a few months down the line is doomed to see a lot of selling pressure. Ideally of course, a working product whether that’s an MVP, testnet, mainnet, a Beta, or a real live working product should be around the corner.

A detailed roadmap and expectation of when a working product will be ready are key requirements whether you’re investing at ICO stage or after.

There’s really no point to have your money parked backing a research project, you want something that’s going to hit the market soon or at least is going to have some kind of impact on the space and start creating value. Some even go as far as not investing in ICOs that don’t have a minimal viable product and that’s the best way to go. The communication and marketing prowess of the team to present the developments of the project in a clear, concise, and optimistic way is also key. Many teams think they should just put their headdown and work on the tech, but that often ends up being a costly mistake as the tech often requires a network effect and that can’t function without an actively engaged community.

Rule #11: Needing A Real Token Use Case

Sometimes a project will get everything right but the token use case just doesn’t make sense. This is not something that many people talk about as we haven’t really reached that point of the market lifecycle where these tokens actually get used other than for speculative purposes. Many projects try to tie a utility to their token but often times the value of the business and network is not fully translated into the tokens themselves. We’re eventually going to transition into a point where many will have STOs (security token offerings) but current projects have been unable to offer investors any sort of dividend or actual share of the company’s profits because they conducted their ICO in a way to go around rules governing securities.

Realize that ICOs don’t equate to an ownership in the company. So the tokens better have real utility.

So while this rule is not so important currently, in the later stages of the lifecycle of ICOs, this is probably going to be among the most important points and it’s something you should keep in mind.

Rule #12: A Marketing Department That Understands The Double Edged Nature of Marketing

Sprinkled throughout this guide is the reminded that ICOs need a healthy community to thrive. However getting the marketing just right to achieve this whilst not appearing like a empty projects that’s mindlessly shilled is a balancing act. Projects like Tron have grown very rapidly because of their outlandish CEO Justin Sun, but at the same time they do command a questionable reputation in the space. Ripple is another company that does marketing right, but they have not presented themselves to the crypto community in the best light and continue to get many haters in the crypto community to this day.

I do believe the entire world wealth will turn into cryptocurrencies like blackhole and grow much bigger in the future. Cryptocurrency will hit 10 trillion USD market cap before @Apple and @amazon do. We will see. Time will tell. #TRON #TRX $TRX

— Justin Sun (@justinsuntron) September 12, 2018

Some projects like Chainlink have picked up bad reputations because of the practically non-existant nature of their communication and marketing. Yet they still have a cult following on sites like 4chan, so it can really go both ways and there’s no clear working formula. The announcement of announcements and other such methods are artificially tried to generate hype usually result in pump and dumps, and if done repeatedly can result in loss in the integrity of the project. At the very least, projects that have frequent and predictable updates make investors feel at ease that development is on-going and that is a nice minimum baseline to have that even projects as large as ICON realized they need. Usually you can pickup on the skill of the team in this regard during the ICO stage, so you can apply that knowledge to see how they will fare with their marketing post ICO and invest accordingly.

Rule #13: Mind The Red Flags

Last but certainly not least, you should always be looking out for red flags that might appear during the ICO funding process. Always assume something is a scam before you start looking at a project and have them convince you they’re not. This is not anything specific and can take many different forms, but if something doesn’t look or feel right, don’t get FOMO (fear or missing out) and jump into a project regardless, there’s always going to be more opportunities. Some of the possible redflags include: a whitepaper that’s been partially plagirized, a dubious money raising process like an uncapped auction, an over inflated Telegram or Twitter account followed by bots, accusations around the team’s past history, Telegram admins banning people when asked relevant questions, lacking or non-existant GitHub code repository updates, not being SEC compliant or passing the Howey test, breaking legal rules like allowing participants from countries where ICOs are banned and there are many many more.

None of this is financial advicce, but we hope this has given you an idea of what to look out for when investing in ICOs and the points you should research in-depth and be vigilant around. Please remember that ICO investing is extremely risky and only invest what you’re willing to lose – that is probably the most important rule in all of this.